June Hogs and Pigs Report: pandemic, feed costs & Prop 12 impacts on market

Alton Kalo discusses the implications of USDA's June 2022 Hogs and Pigs Report 13 July 2022

13 July 2022

2 minute read

2 minute read

By:

By: Alton Kalo, Chief Economist with Steiner Consulting Group, discussed the results of the Hog and Pigs Report released June 30th specifically addressing future supplies and pricing. Following are his insights:

Report Revisions

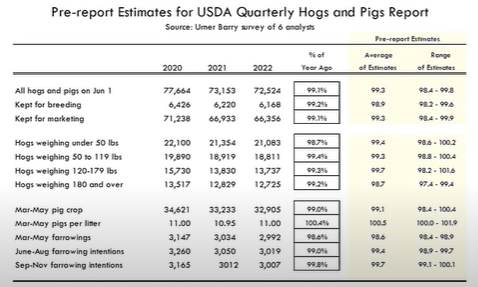

USDA revisions to estimates:

- March 1 market hog inventory revised up 410,000 head or 0.6%

- Pig crop for Sep-Nov was revised up by 411,000 head or 1.2%, attributed to better farrowings

- Pig crop for Dec-Feb was revised up by 123,000 head or 0.4%, attributed to higher farrowings

Report Analysis

Key numbers in the report:

- Total inventory is down 0.9% from last year

- Breeding herd is down 0.8% from last year

- Number of market hogs is down 0.9% from last year

Weekly hog slaughter trends:

- Experiencing usual seasonality: higher in the fall and winter, lower in the spring and summer

- Early to mid-July is 0.8% lower than last year; weekly slaughter is a little ahead of USDA estimates

- Mid-July through late August expected to have 0.7% lower supplies: about 10,000-15,000 head less than last year

- September through early October expected to have 0.6% lower supplies than last year

- Mid-October through late November expected to have 1.3% lower supplies: about 30,000-35,000 head less than last year

Hogs kept for breeding - quarterly inventory:

- Breeding herd dropped about 7% from December 1st, 2019 to March 1st, 2022 due to the pandemic and higher feed costs

- Breeding herd is about 1.1% lower than last year: about 6.168 million head

- About 70,000 head higher than in March 2022

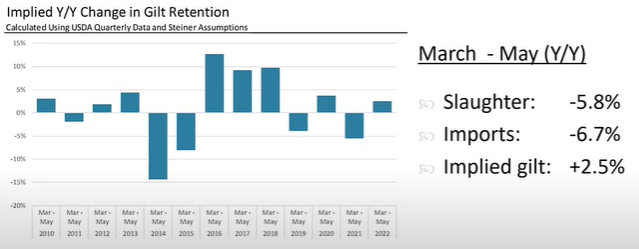

Y/Y change of gilt retention:

- Implied gilt retention is about 5% lower than last year

- Actual gilt retention is 2.5% higher than last year due to herd liquidation, producers profiting February through May ($25/head) even with higher feed costs, and Proposition 12 coming into play

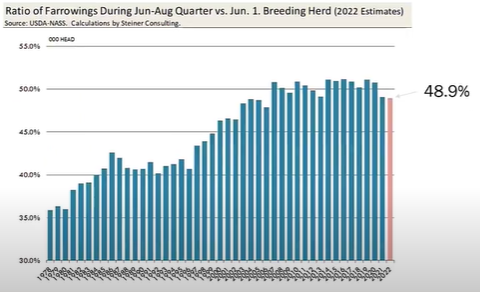

Ratio of Jun-Aug farrowings to June 1 inventory:

- June-August pig crop helps predict the expected supply in December-February

- Ratio of farrowing cases to breeding herd on June 1st was 48.9%

- Farrowing intentions are lower compared to 2021

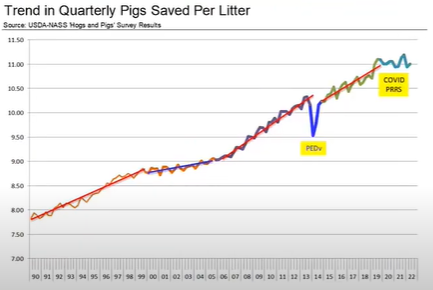

Productivity measures - pigs per litter:

- Producers can improve the productivity by farrowing better or having more pigs per litter

- Upward trend for the past 30 years in number of pigs saved per litter

- In the last couple years, the number of pigs saved per litter has flattened out due to the pandemic and ongoing pig disease pressure

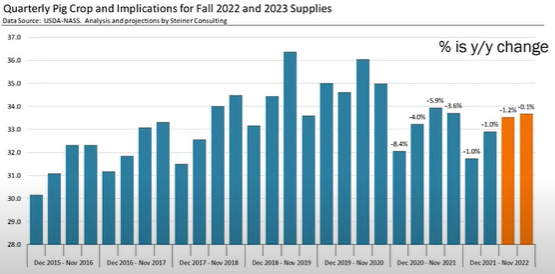

Pig crop for Mar-May and expectations for Jun-Aug and Sep-Nov:

- March-May pig crop was down 1% from last year

- June-August pig crop is expected to be down 1.2% from last year

- September-November pig crop (will go to market next spring) is expected to be similar to last year

Kyle Baldwin

Kyle is a student at the University of Illinois Urbana-Champaign majoring in Environmental Sciences.